How can you maximize your social security bend points?

Do you want to retire early but still get as much social security as possible?

If so, you should understand the bend points of social security. Most financial planners don’t even understand the bend points. But the long and the short of it is that not every year worked has the same payout to you in SS benefits!

What are the social security bend points, and how many years do you need to work to maximize them?

If you haven’t checked on the new SSA.Gov website yet, it is worth checking. Sign in and claim your account!

Social Security Wage Base Impacts Bend Points

Let’s start with a few introductory comments because you need to understand a little about social security before we can go right to the bend points.

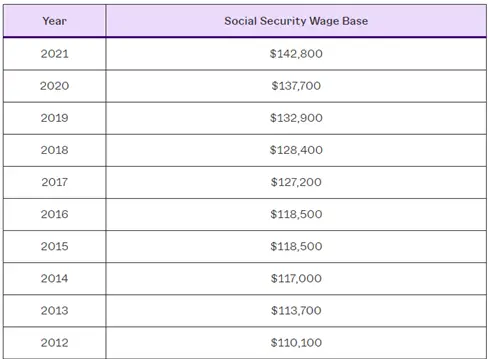

First off, meet the social security wage base. Each year, there is a limit after which you stop paying FICA taxes, and you accumulate no further Social Security benefits even if you make more money.

Some folks don’t understand that Social Security maxes out each year; they think if they earn $800k, they are paying Social Security taxes on the whole amount. (I often see this mistake when people work a W-2 and a 1099. If their W-2 pays out above the wage base, then they don’t need to pay SS taxes on their 1099 side gig.)

You do pay Medicare taxes on the whole amount (1.45% for each employer and employee), but the Social Security tax (6.2% for each) stops at the wage base. So, how much is the Social Security wage base? Well, it changes every year.

Above, you can see the Social Security wage base (the maximum amount you are taxed on for Social Security every year).

You stop paying FICA taxes above the wage base as a high earner. But of course, this also limits the amount of social security credit you earn yearly. That is the point of this blog…. What are the social security bend points, and how do you maximize them even if you retire early?

Now, you understand that you will not max out your social security even if you earn infinity for one year.

Next, we must consider inflation, as money used to be worth more than it is today.

Social Security Index Factors and Bend Points

Social security indexes past wages due to inflation.

Once you are 62, these indexes are set to calculate your AIME. Social security assumes you will keep earning yearly income unless you are 62. If you retire early, you cannot use the AIME or PIA numbers they provide; you must calculate them yourself (since you won’t keep earning income). Once you are 62, AIME can go up if you keep working, but it will not go down.

AIME: AIME is Average Indexed Monthly Earnings. It takes your top 35 index-adjusted years and then applies that to the bend points in order to calculate your PIA.

PIA: PIA is primary insurance amount. It is the monthly benefit you might be eligible for (which is decreased if you file early, and earns delayed retirement credits if you delay filing social security).

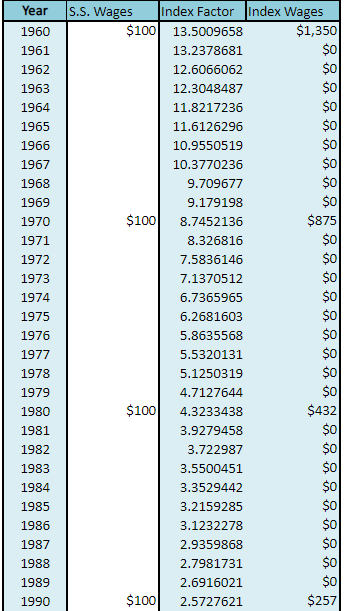

Okay, back to the social security index factors: What has $100 of income been worth toward your AIME over the past decades?

Above, you can see the index factor used when multiplying past incomes.

Note that $100 earned back in 1960 is the same as an income of $1350 in today’s dollars (its index factor is 13.5 and change). Another way to think about this is that, at least according to social security, your money is worth 13.5 times less now than it was 60 years ago. It’s good to know that.

Look through the decades: how much is $100 of earnings worth? Next, note the decrease in the index factor. The index factors change every year (until you are 62, then they are set for you) depending on the amount of inflation each year. The index factor has been stuck at 1 for the last three years.

To finish up above, here are the rest of the numbers. In 2000 you get $168, in 2010 it is $130, and since the index factor is 1 in 2020, $100 is worth $100.

In summary, the wage base was smaller in the past, but to consider inflation, you multiply it by an index factor.

Isn’t social security fun?

Finally, we are ready to get to the bend points.

What Are Social Security Bend Points?

So, what are social security bend points? These are the points when AIME starts paying you less.

How it works: the first dollars you contribute to Social Security pay you more than the last because of the Social Security bend point percentages.

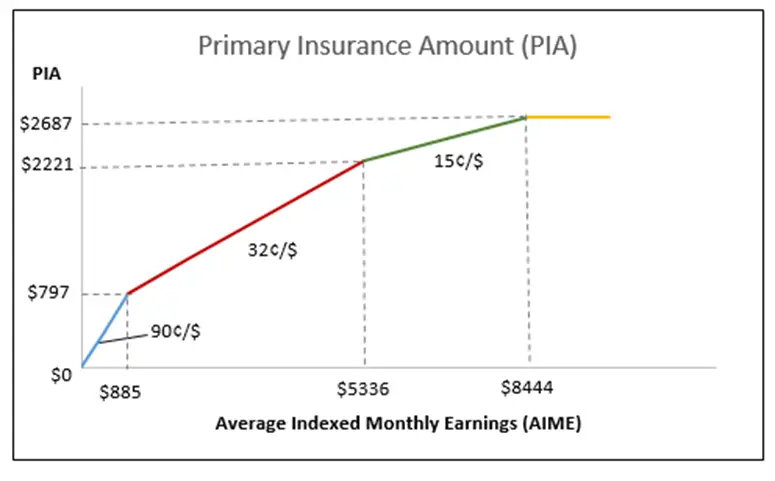

Above, you can see the Social Security bend point graph (which uses 2020 numbers). Along the bottom is your AIME, which is then translated to your PIA.

You can see (blue) that for every dollar of AIME up to the first bend point, you get 90 percent back. Then (red), every dollar provides you with 32 percent. Finally, above the second bend point (green), you get 15 percent; above the max (yellow), any additional amount you pay in social security taxes does not increase your PIA.

Here are the bend point numbers for 2021:

At an AIME of $996, you get 90%. This is the first bend point.

Next, the second bend point is between $996 and $6,002. There, you only get 32% back.

Finally, you only earn 15% of your AIME above that amount. And above $11,900 (the third bend point), you no longer increase your PIA.

The maximum PIA in 2021 (the largest monthly check you can get) is $2324 at 62 and $3113 at Full Retirement Age. (If you get your delayed retirement credits, then at 70, the maximum check is currently $3895.) In 2023, after a nice COLA adjustment, the numbers were $2572 at 62 and $3627 at FRA. Maximum check at age 70 is $4555 in 2023.

To get the maximum amount, you would have needed to earn the maximum wage base in 1986 ($42,000) and continue to earn above the wage base for 35 years.

So, in summary, the first few dollars you earn in social security credits are valuable to you, as you get 90% credit for them. After that first bend point, you only get 32% to the second bend point and 15% above that until you hit maximum social security.

On to the main point of the blog: how many years does it take a high earner to get to their first and second bend point?

How Many Years Does It Take to Get to the First Bend Point?

How many licks does it take to get to the center of a tootsie roll pop? Or, more accurately, how many years do you have to be a high-income earner to hit the first bend point?

The answer is 3. After three years of maximal earning (using the three most recent years with an index factor of 1), you have an AIME above $966.

So, in summary, during the first three years of being a high-earner, you get back 90% of the money you put into social security. The Social Security bend point percentage in your first three years of work is 90%.

Of course, you need 40 income credits to be eligible for social security. Since you can get four credits a year, you must work for at least ten years to get any (personal) Social Security benefits.

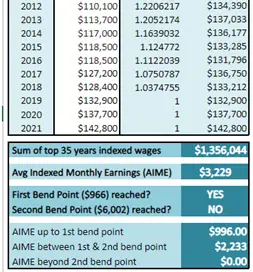

Let’s look at where you fall in the breakpoints after ten years.

Bend Points After 10 Years

Where are we in the bend points after ten years?

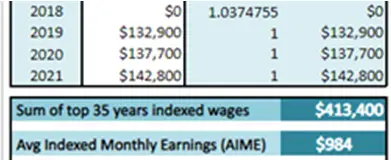

Above, you can see we have earned ten years’ worth of income above the wage base.

Our AIME is $3229, well below the second bend point at $6002.

Because we have a second here, check the index wages on the far right. Note that each year is slightly different, as the wage base and index factor change yearly. Each year’s average is about $135k of wage per year, which counts toward your social security over time.

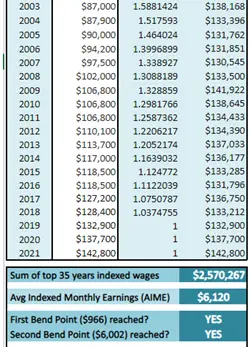

Let’s look at another example: How many years of above-the-wage base earning does it take to hit the second bend point?

How Many Years Does It Take to Hit the Second Bend Point?

So, how many years do you have to work a high-paying job to hit the second bend point?

This is important to understand as you only get credit for 15 cents on every dollar contributed after this point.

Above, you can see that it takes 19 years to hit the second social security bend point.

For a high-income earner, from year 20 to 35, you only get 15 cents credit for every dollar you contribute to Social Security. To me, that is a pretty good reason to retire early!

I want to thank Physician on Fire for his bit on bend points. The Graphs above can be found on his blog.

Summary: How can you maximize your social security bend points?

In summary, you get full credit (90 cents on the dollar) for the first three years you work above the wage base.

Then, you get 62 cents per dollar from years 4-19. For years 20-35, you get 15 cents.

Working an extra year is worth getting your AIME above the first bend point. Once you are past the second bend point, it may be time to find a different job.

Remember, to maximize social security your should build a bridge and claim at 70 to get the delayed retirement credits.