Fungible and Asset Location

Money is Fungible. Fungible is a funky financial term.

Fungible means interchangeable. Or substitutable.

A dollar bill in D.C. is the same as anywhere else. Indeed, $10 is worth two five-dollar bills or ten one-dollar bills. Money is fungible.

Commodities are fungible. You can take sugar from the little bowl and scoop it into your coffee. Since sugar is fungible, you refill it from the jumbo bag you got from any store. Gas is gas at the corner station or the kitty corner where you usually go. Commodities are fungible—that’s what makes them a commodity!

During retirement, money is fungible. If you sell equities from any account to provide income, you can buy equities in a different account and keep your asset allocation on target. Same with bonds.

Even if the market is down and you “sell low,” you haven’t lost if you buy the equivalent “low” in a different account because of fungible money.

Let’s dig in a little deeper to understand how money is fungible. And let’s discuss how a lack of understanding regarding fungibility may lead to mental accounting… and poor asset location.

Money is Fungible, and Asset Allocation

So, how is money fungible regarding asset allocation? How can you withdraw money from any account and keep your asset allocation spot-on?

Say it is time for you to take 4% of your retirement nest egg out to spend. You are under 59 and 1/2, and to avoid the 10% penalty on your qualified retirement accounts, you take money out of a brokerage account.

For convenience, say you have 50% of your money in a brokerage account—100% equities—and 50% in an IRA. Your overall asset allocation is 80/20, so the stock/bond ratio in your IRA is 60/40. If you sell stocks in your brokerage account, you must sell bonds and buy stocks in your IRA to make your asset allocation 80/20 again.

The net effect is due to money’s fungibility: you sell stocks and bonds (at an 80/20 ratio!). You sold stocks in your brokerage account and sold bonds to buy back the same stocks in your IRA. As money is fungible, you kept your overall asset allocation intact!

How does this work in up and down markets?

Selling in an Up Market

Here, say equities have been on a killer run, and your asset allocation has drifted such that it is now above 80/20. As you need to take a distribution anyway, you can sell off equities in your brokerage account and be done with it. Re-balance in your IRA if needed.

Money is Fungible in a Down Market

On the other hand, won’t you be selling your equities low in a down market? Yes, you will. But remember, you can turn around in your tax-deferred account and, without tax liabilities, re-balance there.

So, you sell stocks low, but to return to your pre-determined asset allocation, you sell bonds (hopefully keeping their value) and buy low stocks. In effect, you are not selling low; you are selling bonds!

Thus, as cash is fungible, it doesn’t matter which account you keep your equities or bonds. That is true when you think about asset allocation but not asset location!

Asset Location and Fungibility

Asset Location looks at the tax efficiency of your asset allocation. To keep things simple, we will stick with stocks and bonds.

You must pay ordinary income taxes on short-term capital gains and dividends in your brokerage account. This is why you prefer equity index funds with low turnover (no short-term capital gains). Also, bonds pay dividends taxed as ordinary income in your brokerage account. So, bonds should probably go into your tax-deferred account rather than your brokerage account.

Your other two account types are tax-sheltered (pre-tax and tax-free). You can buy and sell and have all the short- or long-term gains you want, and you won’t have to pay taxes now.

Since money is fungible, asset location means you want tax-efficient funds in your taxable brokerage account and tax-inefficient funds in your tax-sheltered accounts. These are fundamental principles of asset location. If you need more help, visualize the 3-fund portfolio across your account types.

So, in summary, you have different types of funds in accounts with different tax treatments. Because money is fungible, it’s all good! Just swap out stocks and bonds—or re-balance—in the tax-deferred accounts where you can buy and sell without triggering ordinary income or capital gains.

Debt and Fungibility of Money

Because debt is money owed, it is also fungible. Debt is fungible!

Debt is also part of your asset allocation and has a negative or inverse effect.

Say you owe $100k on the mortgage and have $100k in stocks and $100k in bonds. Because debt is like a negative bond, your asset allocation is not 50/50; it is 100/0. The negative $100k in debt wipes away your bonds, and you are taking more risk than you might realize.

You take more risk because you use leverage (borrowing money) to invest in stocks and bonds.

In retirement, not having a debt payment is the same as spending more money. Debt and cash are fungible. If you didn’t have that mortgage, you’d have more money at the end of the month. In addition, debt is leverage and inversely affects your asset allocation. Fun stuff!

Money is Fungible, and Mental Accounting

Here is the heuristic that causes all the problems with the fungibility of money.

Folks don’t think money is fungible. Households don’t treat money as fungible. They use mental accounting instead.

We are subject to mental accounting.

Mental accounting is an essential concept in behavioral economics, most associated with Thaler. It implies that people are disposed to think about an asset’s relative value rather than its absolute value.

Say you have a diamond ring with the same street value as your neighbor’s wedding ring. Are they the same to you?

For example, why do folks spend more on a credit card than they do if they have to pay cash? Or gamble more aggressively with “house money” than with “their own” cash?

Cognitively, money is not fungible in our thought processes, as we attach value to it and consider where it came from and its intended use.

This leads us to ignore opportunity costs. For instance, we hold stocks that have done poorly because loss is more painful than gain is pleasurable.

We also dearly believe in the sunk cost fallacy. Money doesn’t care if what you have left results from a bad decision in the past.

Let’s explore mental accounting by looking at bucket plans and dividend-paying stocks.

Money is Fungible Meaning: Why Dividend Paying Stocks Don’t Make Sense

With dividend-paying stocks, people think they can “live off the interest,” which is safer than a total return approach where you sell funds at capital gains rates when you need the income. Because you are paying ongoing taxes on the qualified dividends rather than choosing when to pay taxes, the dividend approach can be less efficient than the total return approach.

Money is Fungible Meaning: Why Bucket Plans Don’t Make Sense

With bucket plans, people use time segmentation to plan income. They have a cash bucket for “now,” bonds for “soon,” and stocks for “later.” Collapse it all down, and it is just ONE asset allocation. And you still need to address the different asset allocations in different types of accounts to afford tax-efficient asset location!

Risk should be managed across the portfolio, not in a bucket.

Mental Accounting and Asset Location

Let’s return to your brokerage and pre-tax accounts and see where mental accounting affects most folks.

Good tax-efficient asset location suggests that stocks should be in your pre-tax accounts rather than your brokerage account.

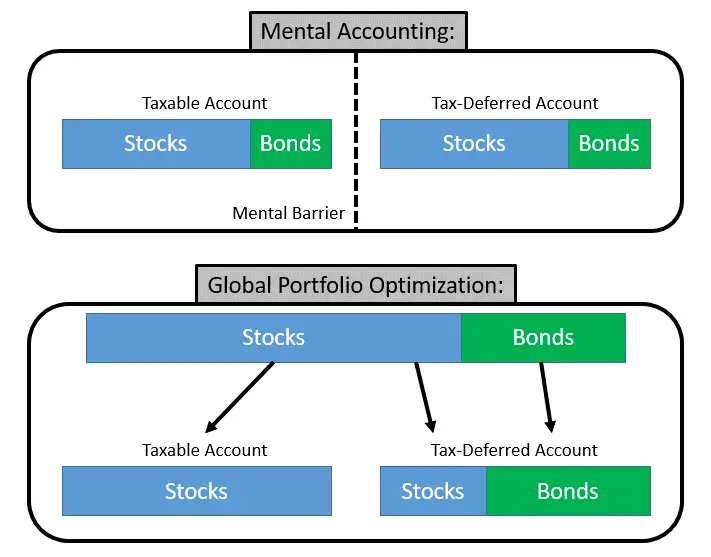

Figure 1 (Money is Fungible, but mental accounting leads to poor asset location)

Mental Accounting leads to poor asset location. Remember, cognitively, we don’t believe that cash is fungible. We ascribe its meaning and purpose depending on where we got it and what we plan for it.

Above Figure 1, you can see the mental barrier between your account types. Here, you have bonds in two kinds of accounts.

However, to optimize taxes, you should hold all tax-efficient stocks in your taxable account and only tax-inefficient bonds in your tax-deferred accounts.

Don’t fear selling low because money is fungible. If you sell low from your brokerage account, you can always change the asset allocation in your tax-deferred account, which nets out as just selling bonds.

Conclusion: Money is Fungible

Money does not come with a label, and there are no tracker tags or collars with specific identification. It is fungible.

Although it is common to bucket money or to create separate accounts, in our mind, you have one portfolio and one asset allocation. Creating buckets of money for separate purposes ignores the fact that money is fungible.

There are many implications: you don’t need an emergency fund, debt is like a negative bond, and you don’t need all cash or bonds in accounts you access sooner than others.

But we don’t live in a rational world. I say if you have blind spots where you ignore the fungibility of money, that is fine. As long as you understand that money is fungible and money doesn’t care where it came from or how you intend to use it.

You don’t have to be perfect, just good enough. As with fungibility and fungi, don’t eat poisonous mushrooms. Eat the edible ones.