Tax Planning Window to Save in Lifetime Taxes

What is the optimal time to do tax management for retirement? The tax planning window!

Not infrequently, that tax strategy is a yearly series of partial Roth conversions. These pre-paid future taxes lock in a tax rate and provide insurance against future tax increases.

The Tax Planning Window is your best chance to pay less in taxes over your lifetime.

The Tax Planning Window

The Tax Planning Window opens after you stop earning income and before you are required to start social security or required minimum distributions (RMDs). This is the optimal time for tax planning for retirement.

For the tax-savvy individual, The Tax Planning Window is a glorious time! There is no other window in time where you have such control over how and when you recognize income. During your tax planning window, you decide exactly how much you will pay in taxes.

Do not ignore your tax planning window for retirement: the goal is to pay the least in taxes over your lifetime. The less you pay in taxes, the more you can spend in retirement or leave as a legacy.

A window is a good analogy because it opens and closes.

Open Window For Retirement Tax Planning

The window opens when you can access your 10 and 12% tax brackets (or sometimes 22 or 24%). This is usually due to retirement, but you can earn less later in your career and take advantage of this retirement tax strategy.

Even better, below the standard deduction, you can access income tax-free.

Use this Tax Planning Window wisely because it closes when you are forced to take income again.

Close Window

The tax planning window closes when you take social security or when RMDs come due.

First, Social Security. Depending on your “provisional income,” you will pay taxes on 50 or even 85% of social security. Half the money you get from social security counts for provisional income, so high earners should assume they must include 85% of their social security as fully taxable. Regardless, at least the high earner in a couple should plan on delaying social security for the longevity benefit, especially if you want a more significant tax planning window. Folks with few assets are hit with the tax torpedo.

Second, you must take the required minimum distributions (RMDs) from your pre-tax accounts. The RMD age went from 70 to 75 (for many) but is 73 for some.

Finally, other sources of income can be recognized as ordinary. For example, pensions and annuities are familiar sources of partially (say, annuities from your brokerage account) and fully taxable income (pensions and annuities from tax-deferred accounts). Remember, there are good annuities that are very worthwhile to consider.

Other sources of income can fill up your brackets. Alimony (before 2018-after that, it stops being a tax deduction), business income (Schedule C), Schedule E income, Schedule F income, Form 4797, and even Capital Gains affect your income.

Capital Gains Stack on Top of Ordinary Income but can negatively affect your Tax Planning Window.

I know this is a lot, but the Tax Planning Window is very important! Let me tell you why.

The Tax Planning Window: the Best Tax Strategy for Retirement

Why?

Control. Yes, you can control how much you pay in taxes.

For a traditional retiree who retires at 65, you have less than five years to access your low tax brackets.

The glory of financial independence is prolonged access to your Tax Planning Window. But, of course, this leads to a whole host of other issues (like what income is most tax-advantaged to live on) that are the bread and butter of FIRE.

Beyond control– flexibility. You get to decide when to do partial Roth conversions.

Partial Roth Conversions: Best Tax Strategies for Retirement

The next best tax strategy for retirement: partial Roth Conversions.

Some people get confused and think there is an income limitation on Roth conversions. There is not. There are limitations on contributions but not conversions.

If you have money in your pre-tax account, you can (usually) press a button to convert it to Roth money, paying taxes now in the year of conversion.

These partial Roth conversions are amazingly powerful! They are among the best tax strategies for retirement.

Having some money in Roth accounts is essential for good tax diversification. It gives you control of future income. Remember the question: to Roth or not to Roth depends on tax rate arbitrage.

Some folks only use their brokerage account during this time, allowing their tax-deferred accounts to grow. This is usually a bad idea, as you will increase the taxes you pay later via RMDs. But, again, the goal is to pay the least taxes over your lifetime. Use the standard deduction and the 10 and 12% tax brackets to pay some tax now to pay fewer taxes in the future.

During the tax planning window, partial Roth conversions can shift this money into tax-free Roth accounts.

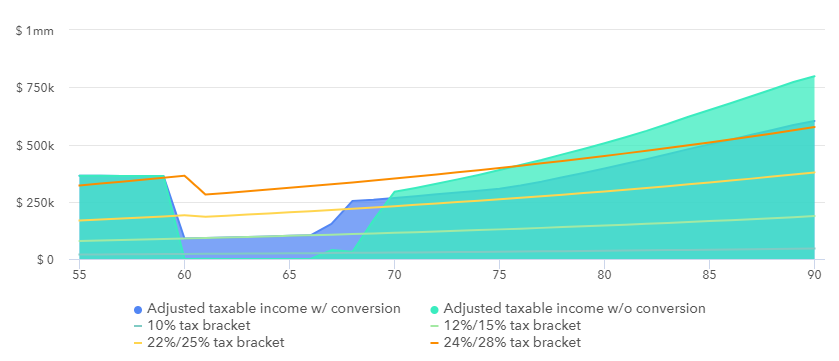

An Example of Partial Roth Conversions

(An example of partial Roth conversions best tax strategies for retirement)

Note that a dark blue shape fills the 10 and 12% tax brackets during the tax planning window. These are the partial Roth conversions!

Also, note that this decreases RMDs and keeps them out of the 24% tax bracket in the future (which will become the 28% bracket once the TCJA expires after 2025).

You pay taxes at very low effective rates during your tax planning window. When you are forced to take RMDs, all of the money comes out “on top” of everything else at your highest marginal tax bracket. Keep your effective tax rate low over your life by decreasing the income included at your highest marginal tax brackets.

Other Retirement Tax Strategies During the Tax Planning Window

What do the best retirement tax strategies offer you? Tax Control and Flexibility!

In your tax planning window, you can reduce future RMDs and accumulate Roth money (so you can withdraw the money without any implications for your taxes), and is efficient tax planning for your Heirs.

What about health care? Controlling your income can get premium ACA tax credits for Obama Care plans. When you reach the age of Medicare, IRMAA is a huge deal. Medicare plans B and D are subject to hefty surcharges if you make too much money.

In the end, it is all about control. Who knows what the future will hold, especially regarding tax rates set by Congress? Do you think taxes will be higher or lower in the future?

Tax Planning for Retirement is your best chance to keep the money you earned rather than pay high taxes.